The Law Offices of

M. FRANKLIN PARRISH

M. FRANKLIN PARRISH

As an estate planning attorney, I meet with numerous clients, each having his or her own unique set of problems and objectives. This area of law is steeped in tradition and primarily deals with married couples and single clients attempting to avoid unnecessary taxation, to avoid problems in asset management in the event of incapacity, as well as probate delays. There are endless articles and books on these traditional married couple and single client issues. However, in my practice, I have increasingly come in contact with same sex couples living together as a family unit, who have failed to do any “proper” estate planning. In most cases, such couples will have all bank accounts, real estate and investments titled in joint tenancy. Likewise, most life insurance will be owned by the insured. These homespun “estate planning techniques” parallel those utilized by many traditional married couples. However, for same sex couples there is not a great deal of literature, either in the popular press or in legal publications addressing the issue of, for lack of a better term, “alternative lifestvle estate planning”. The purpose of this article is to briefly address certain major issues applicable to same sex couples, as well as opposite sex couples living outside of what the law recognizes as a traditional marriage.

Most clients will be surprised that traditional estate planning concepts can be effectively applied in same sex relationships to achieve personal, as well as tax planning benefits. The first issue for such couples to address is: “How are assets titled?” Please understand asset titling not only determines what you can do with your estate, but also what is subject to federal estate taxation. While titling assets as “joint tenancy with right of survivorship” may avoid probate at the death of the first joint tenant/partner, the assets are totally subject to probate in the surviving partner’s date of death. Likewise, joint tenancy may trigger unnecessary federal estate taxation at both partners’ deaths. This is because the Internal Revenue Code requires the total value of all joint assets to be included in the predeceased joint owner’s/partner’s estate, unless the survivor can prove monetary contribution. Therefore, the burden of proof falls on the surviving joint tenant to prove by documentation all monetary contribution. In addition, at the surviving partner’s death, the total value of all assets now titled in that partner’s name will be includable in the estate and again subject to federal estate taxation. Please recall in 2022 the “Applicable Exclusion Amount” applied against any federal estate taxation was increased to $12,060,000, per individual and is now annually adjusted for inflation. In other words, if an estate does not exceed that dollar amount, no federal estate tax is due. However, when calculating the value of assets subject to federal estate taxation most clients fail to realize the face amount of all life insurance on and owned by a decedent, as well as all retirement benefits are included in this amount.

Now in California, the Federal Courts, as well as our State Legislature have legalized same-sex marriages. This opens up entirely new estate tax savings for same-sex couples who are legally married. Same-sex couples now have access the “Unlimited Marital Deductions” for assets passing to a spouse either during lifetime or at death. However, we need to also add into the equation in 2022 the $12,060,000, “Applicable Exclusion Amount” previously addressed. Such amount may now apply to married or unmarried same-sex couples. In addition, federal law looks back to state law when dealing with asset titling. If same-sex couples are legally married, they may also now own assets as “community property”. This offers a major income tax benefit at the death of the first spouse. This benefit is the entire assets’ value, not just the decedent’s one-half (112) ownership interest, receives a new income tax step-up in cost basis when selling the asset. This step-up in income tax cost basis applies to all assets with the exception of IRA’s, cash and annuities. For example, suppose Jim and Joe purchased a residence for $300,000. Subsequently, they get married and re-title the property from joint tenancy to community property. Assume Jim dies ten (10) years later and the residence is now appraised at $1,000,000. If the residence remained titled in joint tenancy only Jim’s one-half (112) interest would receive an income tax step-up in cost basis from $150,000 (e.g., Jim’s one-half of the original purchase price to $500,000). If Joe now sells the property he would be required to recognize gain of his one-half (112) interest in the property (i.e., $500,000 less $150,000, equals $350,000 of taxable gain). However, with “community property” both Jim’s one-half (1/2) interest, as well as Joe’s one-half (1/2) interest in the property receives a one-hundred percent (100%) step-up in income tax cost basis to the new appraised fair-market value of $1,000,000. Now, Joe may sell the property, if he so chooses, and receive $1,000,000 back free of all income taxation. This is the major benefit of “community property” which only exists between married couples, when compared to joint tenancy.

What then is the “proper legal advice” for same sex couple’s federal estate tax dilemma? It all depends upon what they desire to achieve. For example, are they legally married to take advantage of the Marital Deduction or are they living together and are restricted to the “Applicable Exclusion Amount” of $12,060,000, annually adjusted for inflation in 2022. The beginning step, as a general rule is to sever most joint tenancy assets. In the event the clients are not legally married, clients may wish to divide various investments and make them each partner’s “separate property”, or create a “tenancy in common” ownership. A tenant in common is not the same as a joint tenant. Tenant in common interests need not be equal. In addition, at date of death only the deceased partner’s fractional interest is includable in the estate for federal estate tax purposes. Therefore, the amount of assets subject to taxation at the death of the predeceased partner may be cut in half. If that amount is under $12,060,000 in 2022, no federal estate tax return must be filed and no tax is due.

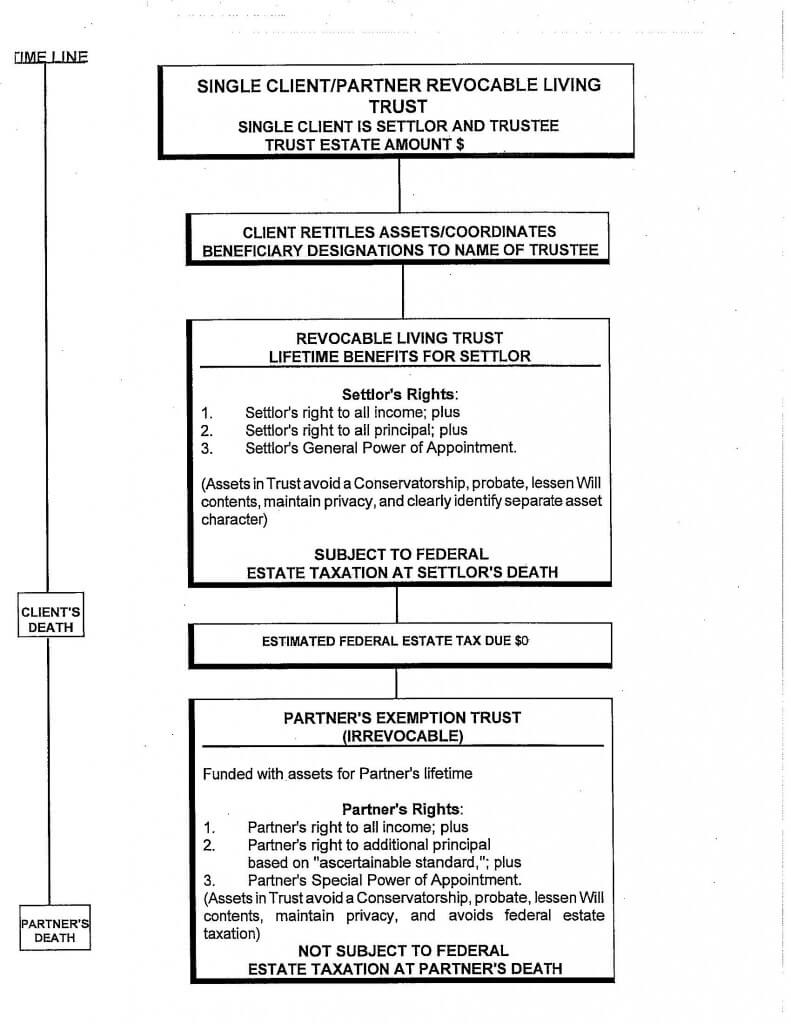

However, the severing of asset titling is only a part of the solution. The next step is for each partner to establish a personal estate plan including, among other documents, a Revocable Living Trust with a tax savings “Sub-Trust” or “Partner’s Exemption Trust”. This planning technique may be used by married, same-sex couples, as well as domestic partners. Rather than leaving all assets including life insurance outright to a partner, such investments may be re-titled or beneficiary designations made payable to The Revocable Living Trust. Each partner is his or her own Trustee. However, at the predeceased partner’s date of death, the surviving partner becomes the Successor Trustee and primary beneficiary of the late partner’s Trust (i.e. now “Partner’s Exemption Trust”). If this “Partner’s Exemption Trust” is properly drafted, the surviving partner may possess the following maximum rights as a lifetime beneficiary without causing the Trust’s asset to be subject to federal estate taxation in the surviving partner’s estate:

I have worked with a large number of same-sex couples and understand their desires. Now, they are on an equal footing with heterosexual couples and can take advantage of the same benefits. The following two (2) pages consist of two (2) different diagrams. The first diagram is used for the trust estate planning concept for an “umnarried” same-sex couple. The second diagram is designed for a same-sex married couple, where the Marital Deduction is fully utilized.